Circular Feeds: The Emergent Reality

Kolmar – A Future Facing Business

• 25years + business pedigree, operates in 22 countries

• The company transacts approximately 6 million metric tons per year with revenues ranging from US Dollars 5 to 8 billion.

• The product portfolio includes Petrochemicals (including olefins, aromatics, petrochemical feedstocks, solvents, alcohols, fiber raw materials), Renewable Fuels (including waste feedstocks, biodiesel, renewable diesel and ethanol), Crude Oil and Petroleum Products (including components) as well as Natural Gas and LNG.

• The business is currently running @ >50% Renewables on a global basis.

• Subsidiary ‘American GreenFuels LLC’ operates a 40M gallon Bio-Diesel refinery in New Haven, Connecticut.

• Currently constructing ‘AGF Rockwood’, 25M gallon Cellulosic renewable diesel, first plant of its kind to produce diesel from wood pyrolysis

• Is a principal investor and sole marketer of Circular Naphtha from the deployment of the Synpet S.A ‘TCP’ technology. 1st Unit deployed in 2024.

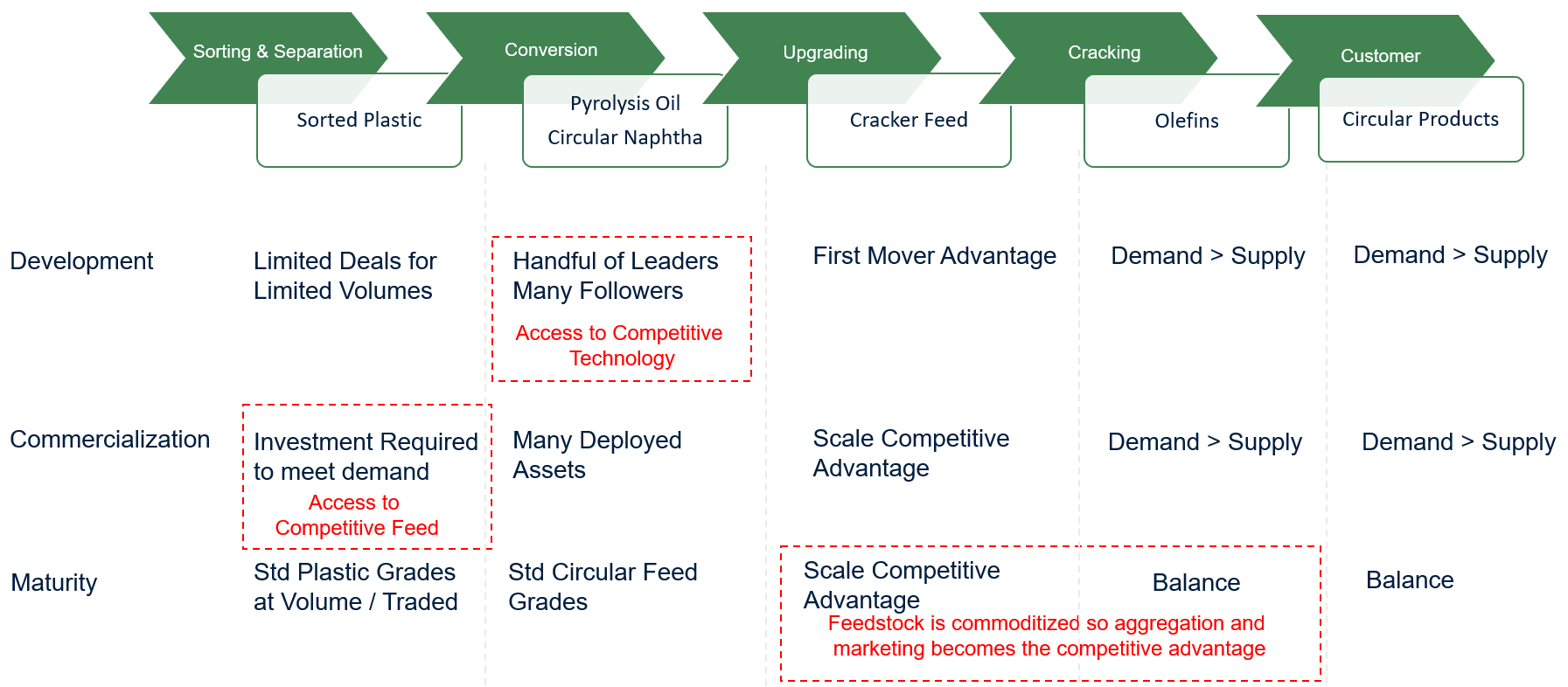

The Management of Plastic Waste & The Chemical Context

The Emerging Realities Of the Circular Value Chain

All is not equal here!

Technology Development & Disruption

Value?

• A value picture is emerging – initial LOI’s [low pricing] moving into offtake commitments

• Formulas under discussion balancing risk and exposures – Naphtha + premium doesn’t mean anything to a circular feed producer.

• Chemical producers need to materialize a market premium to downstream buyers – food packaging is key.

• The circular premium is being carefully guarded, but it will need to distributed to drive upstream supply.

• Quality / Yield will emerge as an important price driver – utility of the product ‘in use’

• Upgrading / No upgrading – prices will reflect the additional processing costs for a cracker operator & ‘straight in’ product should reflect a premium.

• Market is tight, tight, tight – will commoditize over the next decade